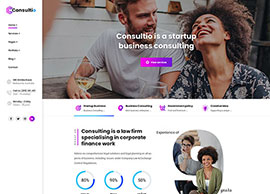

VAT Consultancy

All business in UAEVat Consultancy services for all businesses in UAE

With over 15 years of experience,

we’ll ensure you always get the best financial business solutions.

Accounting

Financial Audits and RERA Audit services.

Financial Audits

RERA Audits

Nadeem and Umendra Chartered Accountants – Best Audit firm in Dubai, emerged as one of the most sought-after service provider in its field meeting various needs and demands of its clients operating in the local, regional and international markets. As its name features on the Approved List of Auditors of local banks and the free zones in the UAE.

We will assign an obsessive auditor for your firm. The experienced auditor can work completely for you. Remaining involved with you perpetually, they’re going to clarify your queries, meet your necessities and clear your doubts.

Consultio comes with a beautiful collection of modern, easily importable, and highly customizable demo layouts. Any of which can be installed via one click.